Save big with aidemoremix deals 20% OFF "remix20"

Decoding Debt: The Ultimate Deep-Dive Guide to Bank Loans

How to work Bank with our money

BANKING

6/10/20264 min read

Loans are often viewed simply as a way to get cash when funds are short. In reality, they are powerful financial instruments. When used strategically, a bank loan can help you acquire appreciating assets, fund life-changing education, or scale a business enterprise.

However, entering a credit agreement without understanding the fine print can lead to financial strain. This comprehensive guide breaks down the major categories of bank loans, how they operate under the hood, and what banks look for during the approval process.

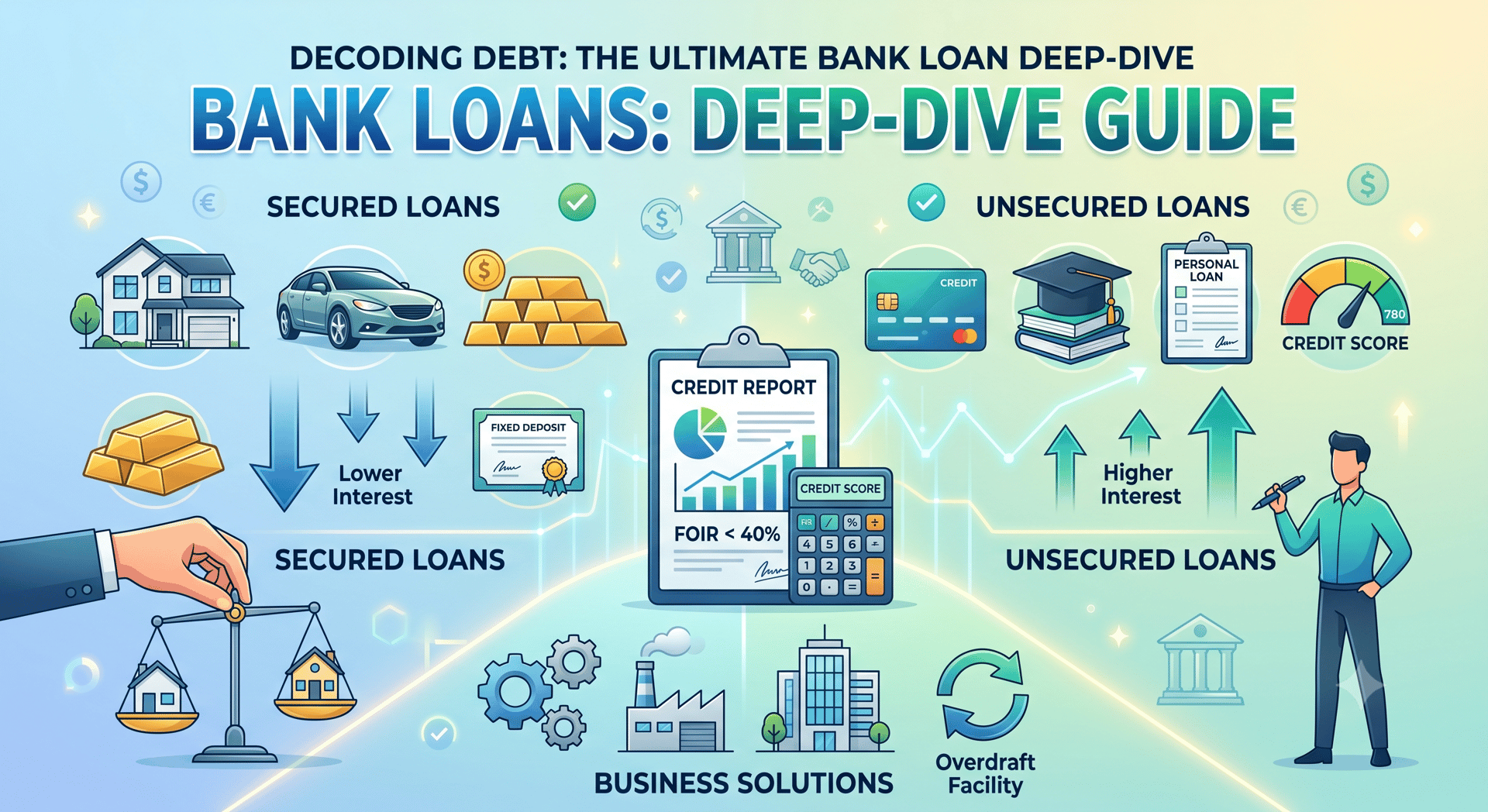

1. The Core Split: Secured vs. Unsecured Debt

Every bank loan fundamentally falls into one of two categories based on how the risk is managed between you and the lender.

Secured Loans: Asset-Backed Borrowing

Secured loans require you to pledge a valuable asset—such as real estate, gold, or fixed deposits—as collateral.

The Mechanics: The bank evaluates the market value of your asset and applies a Loan-to-Value (LTV) ratio (usually ranging from 60% to 90%) to determine your maximum loan amount.

The Advantage: Because the bank can seize and liquidate the asset if you default, their risk is low. This translates directly into lower interest rates and longer repayment tenures for you.

Unsecured Loans: Credit-Based Borrowing

Unsecured loans require no collateral. The bank lends you money based strictly on your financial reputation and capacity to repay.

The Mechanics: Lenders look at your credit history, income stability, and existing debts.

The Advantage: You don't risk losing a specific physical asset if your financial situation takes an unexpected turn, and the approval process is significantly faster. However, because the bank takes on high risk, these loans come with higher interest rates.

2. In-Depth Breakdown of Retail & Consumer Loans

Retail loans are designed for individual consumers to meet personal, family, or household needs.

A. Home Loans (Mortgages)

A home loan is a long-term commitment, typically spanning 15 to 30 years. The property you buy serves as the primary security for the loan.

Fixed vs. Floating Interest Rates: A fixed rate remains constant throughout the tenure, providing predictable monthly payments. A floating rate fluctuates based on market benchmarks (like the central bank's repo rate). Floating rates are often cheaper initially but carry market risk.

Top-Up Loans: If you have been regularly paying off your home loan and the property value has appreciated, many banks allow you to take an additional "top-up" loan at interest rates much lower than a standard personal loan.

B. Personal Loans

The Swiss Army knife of banking, personal loans are unsecured and have no restrictions on how the funds are spent.

Tenure & Costs: Usually repaid over 1 to 5 years. Because they are unsecured, processing fees can be higher, and pre-closure penalties (fees for paying off the loan early) are common.

Best Used For: Debt consolidation, emergency medical expenses, or sudden, necessary expenses that cannot wait.

C. Education Loans

Education loans fund higher studies globally, covering tuition, books, accommodation, and travel.

The Moratorium Period: This is the most unique feature of a student loan. Borrowers are granted a grace period consisting of the duration of the course plus 6 to 12 months. During this time, you are not required to pay full Equated Monthly Installments (EMIs), allowing the student time to graduate and secure employment.

Co-Applicant Requirement: Since students typically lack an income history, a parent or guardian must sign as a co-applicant to guarantee repayment.

D. Gold Loans & Loans Against Fixed Deposits (FD)

These are liquidity lifesavers for short-term crunches. Instead of breaking an investment or selling family gold, you hand them over to the bank temporarily.

Speed: These loans offer almost instant disbursement because the bank already holds an asset of verified value.

Impact: Your credit score matters less here; even individuals with poor credit can secure a gold loan easily.

3. The Engine of Growth: Business & Commercial Loans

For entrepreneurs and enterprises, bank loans provide the necessary leverage to manage cash flow and invest in expansion.

┌─────────────────────────────┐

│ Types of Business Loans │

└──────────────┬──────────────┘

│

┌───────────────────────┼───────────────────────┐

▼ ▼ ▼

[ Term Loans ] [ Working Capital ] [ Overdraft (OD) ]

Long-term capital Day-to-day costs Revolving credit

for major expansion (Inventory, payroll) pay only on used

A. Business Term Loans

Term loans provide a lump sum upfront, which is repaid over a fixed schedule (typically 3 to 10 years).

Purpose: Primarily used for capital expenditure (CapEx)—such as opening a new branch, acquiring another company, or funding massive long-term projects.

B. Working Capital Loans

Unlike term loans meant for growth, working capital loans are designed to manage operational cycles.

Purpose: They bridge the gap between paying for raw materials/inventory and receiving cash from clients. These are short-term loans, often structured to match the business’s specific cash-conversion cycle.

C. Overdraft (OD) Facilities

An overdraft is a revolving credit line linked to a business current account.

The Mechanics: The bank sets a maximum borrowing limit (e.g., $50,000). You can withdraw funds up to this limit even if your account balance hits zero.

The Advantage: You only pay interest on the exact amount you use, for the exact number of days you use it. If your limit is $50,000 but you only pull out $5,000 for a week to clear payroll, you only owe interest on that $5,000 for 7 days.

4. The Bank's Blueprint: How Loans Are Evaluated

To secure approval and negotiate the best possible interest rates, it helps to understand exactly what underwriters look for when reviewing an application.

Evaluation MetricWhat It MeasuresIdeal TargetCredit Score (CIBIL/FICO)Your past track record of handling debt and making timely payments.750 or higherFixed Obligation to Income Ratio (FOIR)The percentage of your monthly income already going toward existing debts.Under 40% to 50%Income StabilityThe consistency of your earnings (salaried employment history or audited business financials).2+ years of steady returnsCollateral QualityThe ease with which an asset can be valued, verified, and liquidated if necessary.Clear legal titles, high market demand

Pro-Tip for Borrowers

Before applying for a major loan, avoid opening multiple new credit cards or taking out minor retail loans. Every formal loan application triggers a "hard inquiry" on your credit report, which can temporarily dip your credit score and signal to lenders that you are credit-hungry.

Ai Demo Remix

Explore our website and connect with us for any help.

Contact

Newsletter

info@aidemoremix.com

+91-9837587735

© 2026. All rights reserved.