Save big with aidemoremix deals 20% OFF "remix20"

How to credit card business work

They make profit because you make mistake

BANKING

6/11/20264 min read

Part 1: How the Credit Card Business Makes Money

The credit card industry is built on a complex ecosystem involving four main players:

The Cardholder: The consumer using the card.

The Issuing Bank (Issuer): The bank that provides the credit card to the consumer (e.g., Chase, Citi, Capital One). They take the risk by lending the money.

The Merchant: The business accepting the card payment (e.g., Starbucks, Amazon).

The Payment Network: The infrastructure connecting the bank and the merchant (e.g., Visa, Mastercard).

Credit card companies (specifically the issuing banks) generate revenue through three primary channels.

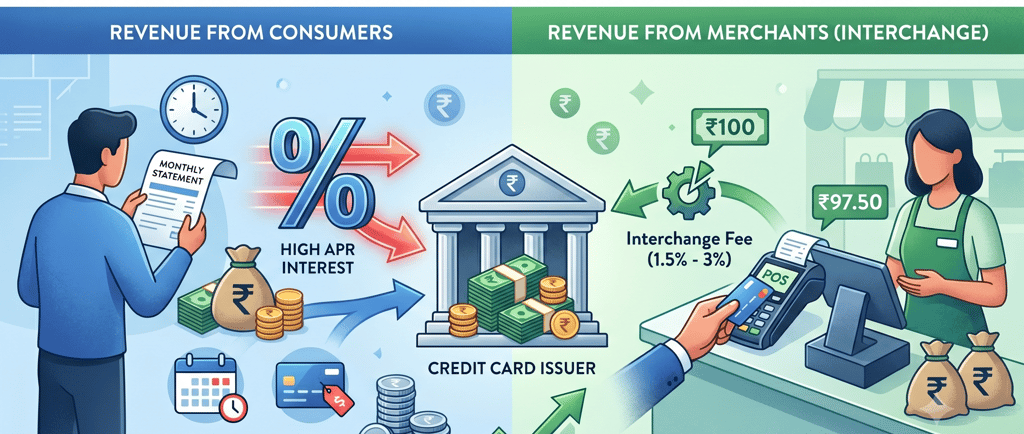

1. Revenue from Consumers (Interest and Finance Charges)

This is often the most significant revenue source. When a cardholder carries a balance from month to month (revolving debt), they are charged Annual Percentage Rate (APR) or interest on that loan.

Average APR: Credit card APRs are typically much higher than other loans (often ranging from 15% to 30%). This makes revolving debt highly profitable for the bank.

Cash Advances: Taking cash out from an ATM using a credit card usually incurs immediately high interest rates and additional fees.

2. Revenue from Consumers (Fees)

Issuers charge consumers numerous types of fees for various actions (or inactions). These add up significantly.

Annual Fees: Fees charged just for the privilege of having the card (often associated with high-rewards cards).

Late Payment Fees: Penalties for missing the monthly payment deadline.

Balance Transfer Fees: Fees charged to move debt from one card to another.

Foreign Transaction Fees: Fees for using the card outside the cardholder's home country.

Cash Advance Fees: Upfront fees charged for taking a cash advance.

3. Revenue from Merchants (Interchange and Transaction Fees)

This is the hidden revenue source that many consumers don't see. When you swipe your card, the merchant pays a fee to accept that payment.

Interchange Fees: This is the bulk of the merchant fee. It's a small percentage of the total transaction value (usually 1.5% to 3.0%), set by the Payment Networks (Visa/Mastercard), but the majority of this fee actually goes to the Issuing Bank that issued the card. This fee helps fund rewards programs and covers the risk of fraud.

Processing/Network Fees: These smaller fees go to the Payment Network (Visa/Mastercard) for facilitating the electronic communication and security between the bank and the merchant.

Part 2: The Blog Post

Swiping Right on Profits: Unveiling How Credit Cards Really Make Money

Have you ever wondered how your "free" rewards credit card, which pays you 2% cash back and includes free airport lounge access, can possibly be profitable for the bank that issued it?

It’s easy to assume that banks only make money when people fail to pay their bills on time and are hammered with huge interest charges. While that is certainly a major cash cow, it is only part of the puzzle. The credit card business model is far more diversified and lucrative than it appears.

In reality, credit card companies have engineered a brilliant system that generates revenue every time you use the card, and every time you don’t pay it in full.

Let’s peek behind the curtain at the two main engines powering the credit card profit machine.

Engine 1: The Money You (The Consumer) Pay

For many consumers, this is the obvious part. If you carry a balance on your card, you are effectively borrowing money from the bank. And banks don't lend money for free.

The Power of Revolving Interest (APR): When you don't pay your full balance by the due date, the remaining amount starts accruing interest at the Annual Percentage Rate (APR). Unlike a car loan or mortgage where the interest rate might be 5% or 7%, credit card APRs are notoriously high—frequently surpassing 20%. This difference makes credit card lending immensely profitable. Even if a percentage of borrowers default, the high interest paid by the rest more than makes up for the losses.

The Nickel-and-Diming of Fees: Even if you pay your bill in full every month, the bank can still profit from your usage. They have designed a whole ecosystem of fees to capture revenue at every turn:

Annual Fees: The cost to hold premium or rewards cards (often $95 to $695+).

Late Fees: Financial penalties for missing your payment deadline.

Cash Advance Fees: Steep upfront charges and higher interest if you use your card for cash.

Balance Transfer Fees: Charged when you move debt from one card to another.

Foreign Transaction Fees: Extra charges for using your card abroad.

Engine 2: The "Hidden Tax" Merchants Pay (The Real Secret)

This is the hidden part that many consumers are unaware of, and it is crucial to understanding the "rewards" ecosystem. Every time you buy something with a credit card, the store (the merchant) does not get 100% of the money. They must pay a processing fee to accept that card.

This fee is called Interchange, and it is the magic behind how credit card companies make money even on responsible consumers.

How Interchange Works: When you spend $100 at a restaurant, the restaurant only receives about $97.50. The remaining $2.50 (roughly 2.5%) is sliced up:

The Majority (e.g., $2.00) Goes to the Issuing Bank: The bank that gave you the card (like Chase or Capital One) gets the largest piece of this pie. This revenue source is why they can afford to offer you that "free" lounge access and "2% cash back." They are paying you using money they took from the merchant.

The Rest (e.g., $0.50) Goes to the Networks and Processors: Visa or Mastercard take a small "network fee" for running the secure electronic plumbing that moves the money. Other small fees may go to the technology company providing the payment terminal.

This means that even if you pay your bill in full every single month and never pay a dime in interest or fees, the issuing bank still made several hundred dollars last year just because you used their card for your groceries and Amazon purchases.

The Ecosystem of Spending

To maximize their interchange revenue, banks have created the ultimate incentive structure: The Rewards Program. By offering lucrative travel points or cash back, banks encourage consumers to put everything on their cards rather than using cash or debit. The more you spend, the more the bank collects in interchange fees from merchants.

The Bottom Line:

The credit card business is not dependent on consumers making mistakes. It is a highly resilient machine with multiple gears:

It profits from revolving debt (interest).

It profits from consumer habits and mistakes (fees).

It profits from every transaction made (interchange).

For consumers, the key to winning this game is simple: Treat your credit card like a debit card. Use it to collect rewards (using the merchant’s money), but always pay your full balance every single month to avoid letting Engine 1 (the interest engine) eat those profits.

Ai Demo Remix

Explore our website and connect with us for any help.

Contact

Newsletter

info@aidemoremix.com

+91-9837587735

© 2026. All rights reserved.